Mortgage Rates

Not only do rates affect buyers, but they also impact the number of sellers.

Just about everyone loves the beach. Basking in the sun, walking along the coast, listening to the soothing sounds of waves crashing on the shore, and taking a refreshing plunge in the cool, salty water, are some of the many reasons so many head to the beach, especially on the weekend. Yet, what happens when it is overcast and cool during the winter? Not as many Southern Californians make the pilgrimage to the beach. There are still plenty of beachgoers when it is cool, from die-hard surfers in their winter wetsuits to locals taking a walk or jogging on the sand. Still, there is a definitive difference between the hot summer days and the crispy winter weather with the wind blowing and temps in the 50s. There are times when beaches seem almost deserted.

Similarly, when mortgage rates are low, the market heats up with a rise in affordability and buyer demand, along with a surge of homeowners desirous of taking advantage of a great time to make a move. Yet, when mortgage rates substantially rise as they did over the past year, demand diminishes due to affordability constraints, and many sellers opt to “hunker down” as they enjoy their underlying, locked-in, low fixed-rate mortgages.

The pandemic was an enormous disruptor, and housing benefited profoundly due to the involvement of the Federal Reserve and the Federal Government. The Fed brought the Federal Funds Rate to zero and bought trillions of dollars of both mortgage-backed securities and treasuries. Mortgage rates dropped to record low levels, instigating tremendous housing demand. The Federal Government passed stimulus packages that sent checks directly to United States citizens. Bank accounts swelled and enabled many buyers to achieve their dream of homeownership. Mortgage rates remained at unbelievably low levels, and housing benefited with a nearly instantaneous, insanely hot market that lasted for two years, from June 2020 to May 2022. That is when the Federal Reserve stepped in and started hiking rates and reducing the number of mortgage-backed securities on their books. Mortgage rates soared, and the Fed slammed on the housing market’s brakes.

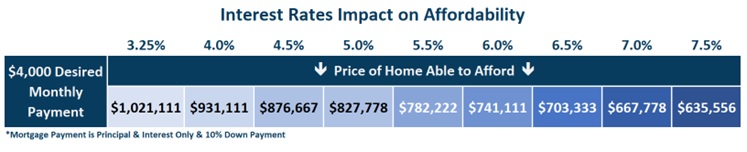

In 2022, mortgage rates started the year at about 3.25%, according to Mortgage News Daily, and surpassed 7% in both October and November. It was a constant erosion of purchasing power for buyers looking to purchase. Last year’s giant jump in rates had a significant impact on affordability. For example, buyers desirous of a $4,000 per month principal and interest payment with 10% down started the year looking at a $1,021,111 home. By October, with rates above 7%, the same buyer was looking at a $665,000 home.

Understandably, rising rates sideline many buyers. Yet, since November, mortgage rates have remained below 7% with duration, inviting many buyers to begin their search for a home again. They averaged 6.3% in December, 6.2% in January, and 6.5% thus far in February. Recently, a series of positive economic reports, which is not helpful in the Fed’s inflation fight, has resulted in rising rates, reaching 6.87% today.

Nonetheless, as the economy eventually slows, mortgage rates are anticipated to fall. As they fall, affordability will improve, and demand will rise. In looking at that same desired $4,000 monthly payment, a drop from 7% to 6% allows a buyer to increase their search from a $667,778 home to one at $741,111. Rates could reach 5.5% in the summer if inflation falls and the economy cools, which would allow that buyer to broaden their search to $782,222. As rates drop, affordability improves, allowing more purchasers to enter the housing arena.

Higher rates sideline many sellers as well. Some homeowners would like to move but choose to “hunker down” and stay put instead. Their current underlying low, fixed-rate mortgage is preventing them from selling. Since 89% of all California homeowners with a mortgage have a rate at or below 5%, and 71% have a rate at or below 4%, the higher rate environment limits the number of sellers coming on the market. In Los Angeles County in 2022, there were 16% fewer sellers, nearly 15,000 missing FOR-SALE signs due to the hunkering down trend. In January, there were 34% fewer sellers, or 2,517 missing signs. That is a big chunk of the housing market. As rates drop, the gap between a homeowner’s underlying rate decreases. When rates eventually drop below 5.5%, that gap will narrow enough to entice many homeowners to sell, and fewer homeowners will continue to hunk down.

The missing sellers have resulted in a falling inventory despite lower demand levels. Demand, the last month of pending sales activity, is at 3,763, readings last seen during the May 2020 lockdowns of the pandemic. Yet, there are only 7,600 homes available today, an anemic reading well off the 3-year pre-pandemic average for mid-February (2017 to 2019) of 10,806 homes, 42% higher than today. As a result, the market feels exceptionally hot even with higher rates with an Expected Market Time, the time between listing and successfully negotiating a contract to sell, of only 61 days. The 3-year pre-COVID average was 65 days. Today’s hot market is a function of the low supply and fewer homeowners coming to market, not record-breaking demand.

Mortgage rates pave the path for housing. Substantially higher rates have been limiting supply and demand, constraining the number of closed sales. As rates drop, demand rises, more homeowners opt to sell, and more closed sales will occur.

The Luxury Market Notched at Least Seven $100 Million Deals in 2022 (copy)